Wholesale Real Estate Contract: Free PDF Template (2026)

Jun 02, 2026

Written by

Alex Martinez — Founder & CEO, Real Estate Skills. Has wholesaled and flipped houses for over a decade, personally acquiring 33+ residential investment properties.

Reviewed by

Ryan Zomorodi — Co-Founder & COO, Real Estate Skills. Reviewed and verified the contract walkthroughs, assignment process, and legal points in this guide before publication.

Publication history: Originally published April 27, 2021. Updated June 2026 with line-by-line contract walkthroughs, current assignment-fee figures, an updated FAQ, and added guidance on assignment vs. double closing and state-by-state legality. Contract walkthroughs verified by Ryan Zomorodi, Co-Founder & COO of Real Estate Skills.

A wholesale real estate contract is the paperwork that lets you lock up a property and sell your right to buy it for a fee. It's really two documents: a Purchase & Sale Agreement between you and the seller, and an Assignment Contract that transfers your position to a cash buyer. You never own the property and you get paid an assignment fee, typically $5,000 to $20,000, for putting the deal together.

Most people who fail at wholesaling don't fail because they couldn't find a deal. They fail because they didn't understand the wholesale real estate contracts. They lock up a property, can't find a buyer in time, and panic because they have no idea whether they're on the hook to buy it, whether they can get their earnest money back, or how they were supposed to get paid in the first place.

That's the whole game right there. A wholesale deal lives or dies on two pieces of paper. Get them right, and you control the deal, you're protected if it falls apart, and you get paid even when things go sideways. Get them wrong, and you're exposed, or you watch a good deal collapse because of one clause you didn't understand.

So that's what this is. I'll walk you through both contracts line by line: what every section means, how to fill it out, and the parts that actually matter versus the boilerplate you can skim. These are the exact contracts I use in my own deals and that thousands of our students have used to wholesale across the country. You can download them free here and follow along.

FREE Wholesale Real Estate Contracts (Walkthrough)!

Ryan Zomorodi walks through how to use and fill out both wholesale contracts (the Purchase & Sale Agreement and the Assignment Contract) so you can lock up your next deal with confidence.

What Is A Wholesale Real Estate Contract?

A wholesale real estate contract is a legal agreement that gives a wholesaler the right to buy a property and assign that right to another buyer for a fee. It works through two documents: a Purchase & Sale Agreement with the seller, and an Assignment Contract that transfers the deal to a cash buyer. The wholesaler never takes ownership.

In plain terms, the wholesaler is the middleman. You find a deal, sign a Purchase & Sale Agreement (PSA) with the seller, then hand your position to an end buyer using an Assignment Contract. You get paid the difference: the assignment fee.

Here's something most beginners get wrong, and it matters: until you assign the contract, you are the buyer. When you sign the PSA, the law treats you as the person buying that house. You're not "sort of" in the deal; you have a real, legally binding obligation to perform, and a real equitable interest in the property. That's exactly why it works: that interest is the thing you're selling when you assign. So go in with genuine intent to buy, but you've been warned: a contract you can't actually perform on is a flimsy one.

💡 Quick Example: How A Wholesale Contract Works

- You sign a PSA with a seller to buy their property for $120,000.

- You bring the deal to a cash buyer who agrees to take it.

- You use the Assignment Contract to assign your right to buy it to that cash buyer for $135,000.

- The buyer closes directly with the seller, who gets their $120,000.

- You collect the $15,000 difference as your assignment fee — without ever owning the house.

Two documents do all the work in a wholesale deal. Here's how they compare at a glance:

| Purchase & Sale Agreement | Assignment Contract | |

|---|---|---|

| Who signs it | You (the wholesaler) and the seller | You (the assignor) and the cash buyer (the assignee) |

| What it does | Locks up the property so the seller can't sell to anyone else | Transfers your right to buy the property to the end buyer |

| When you use it | First — to control the deal | Second — once you have a buyer lined up |

| Length | Several pages — the full terms of the purchase | Usually one page — short and simple |

| How it pays you | It doesn't directly — it establishes your interest | This is where your assignment fee is set and collected |

Master these two documents, and you can wholesale with confidence. The rest of this guide walks you through filling out each one, line by line.

What Makes A Wholesale Contract Legally Binding?

A wholesale contract is legally binding when it has five elements: an offer, acceptance, consideration, legal capacity of both parties, and a lawful purpose. Miss one (most often a missing seller signature) and the contract can be void and unenforceable.

A wholesale contract isn't special in the eyes of the law. It's a real estate purchase agreement, and it has to hold up like any other contract. Five things make it enforceable:

| Element | What It Means In A Wholesale Deal |

|---|---|

| Offer | You present a written offer to buy the property at a specific price and terms. |

| Acceptance | The seller signs and accepts. Every owner on title has to sign — miss one, and it's void. |

| Consideration | Something of value changes hands — usually your earnest money deposit. |

| Capacity | Both parties are legally able to contract — of age, sound mind, and authorized to sign for any entity or trust. |

| Legal purpose | The deal is for a lawful transaction — a normal property sale. |

The one that trips people up is acceptance. If a property has multiple owners (husband and wife, business partners, a few heirs who just inherited it), every one of them has to sign. Fall one signature short, and your contract can be worthless. So before you write the offer, do a little title research or call a title company and confirm exactly who owns the property and who needs to sign. This part is not optional.

One more thing worth saying plainly: state laws differ on what disclosures and wording a wholesale contract needs, and that's not something to wing. Use a proven contract template built for wholesaling in your specific state, and have a local real estate attorney review it before you use it, especially your first time.

How To Fill Out The Purchase & Sale Agreement (PSA) For Wholesaling

To fill out a wholesale Purchase & Sale Agreement, you complete the parties, property, and price sections, set your earnest money and inspection contingency, and include "and/or assigns" language so the contract is assignable. Then get every seller's signature to make it binding.

The Purchase & Sale Agreement is the most important document in any real estate deal: wholesale, flip, or buy-and-hold. On a listed property, an agent usually fills this out for you. But when you're buying directly from a seller, you fill it out yourself, and you want to do it with confidence. I'm going to skip the fine print and cut to the parts that actually matter in a real deal.

A note before we start: this walkthrough is educational and explains how these clauses generally work — it isn't legal advice. Contract forms and requirements differ by state, so confirm the specifics with a licensed real estate attorney before you sign or submit anything.

Wholesale Real Estate Contracts: How To Fill Out (FREE CONTRACTS)!

Ryan Zomorodi walks the Purchase & Sale Agreement and Assignment Contract line by line — every clause explained in plain English so you can fill them out yourself.

Here's the whole agreement at a glance — what each part does and what you put in it. Then we'll go through the ones that matter, one by one.

| Section | What It Does | What You Put In It |

|---|---|---|

| 1. Parties | Identifies buyer and seller | All sellers' names + the "and/or assigns" buyer line |

| 2. Property | Identifies the subject property | Address + APN + property type |

| 3. Included in price | Lists what conveys with the sale | Fixtures (auto) + any personal property you negotiate |

| 4. Purchase price | Sets price and how it's paid | Total price, EMD in 4B, "cash" in 4E |

| 5. Earnest money | Says where the deposit goes | Nothing — confirms it goes to title/escrow, not the seller |

| 6. Financing | Financing contingency | Cross it out on a cash offer |

| 7. Condition | Liability release | Nothing — standard language |

| 8. Inspection | Your main protection clause | A 7–14 day inspection window |

| 9. Lead paint | Required disclosure (pre-1978) | Nothing — standard |

| 10. Closing & title co. | Sets closing date + title company | Closing date + "buyer's choice" for title |

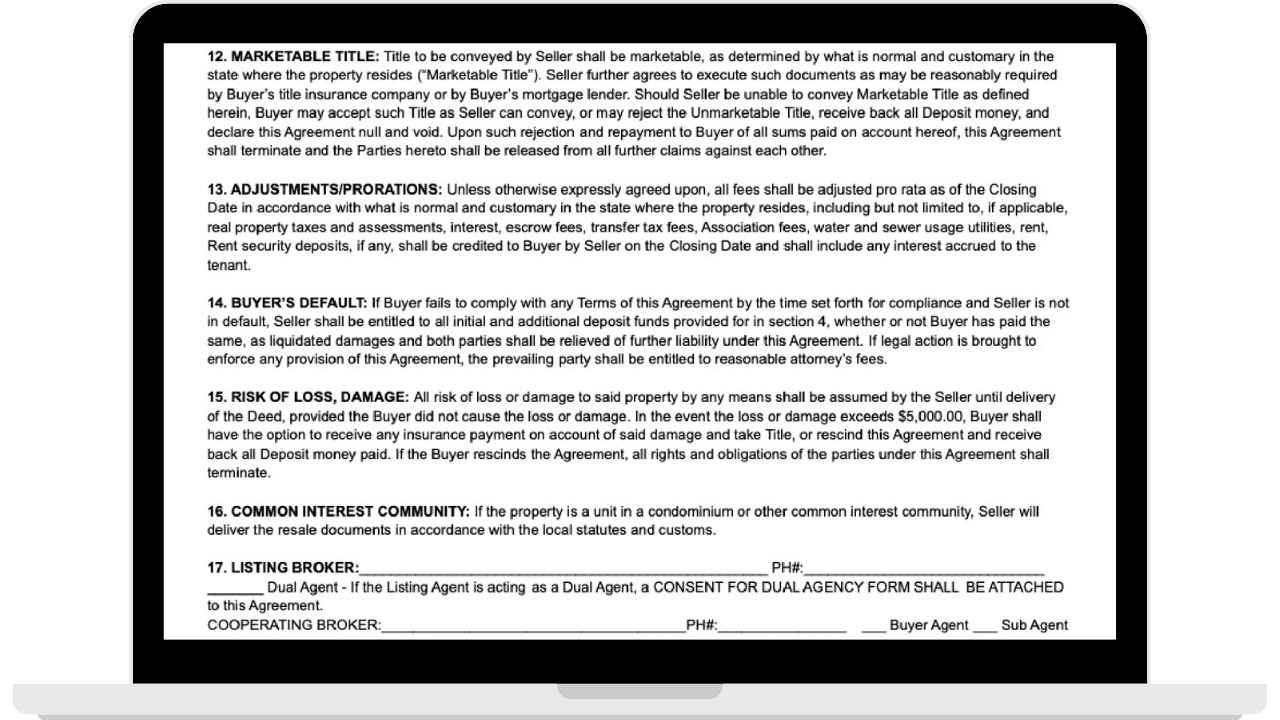

| 11–12. Deed & title | Guarantees clean, marketable title | Nothing — acts as a title contingency |

| 13. Prorations | Splits taxes/rents at closing | Nothing — title handles it |

| 14. Buyer default | Caps your risk (liquidated damages) | Nothing — confirm it's there |

| 15. Risk of loss | Protects you if property is damaged | Nothing — standard protection |

| 16–24. Disclosures | Standard disclosures + boilerplate | Broker info in 17 if applicable |

| 25. Marketing clause | Your right to market the deal | Nothing — but make sure it's in there |

| 26–30. Close-out | Short sale, license, deadline, signatures | Deadline to accept + all signatures & initials |

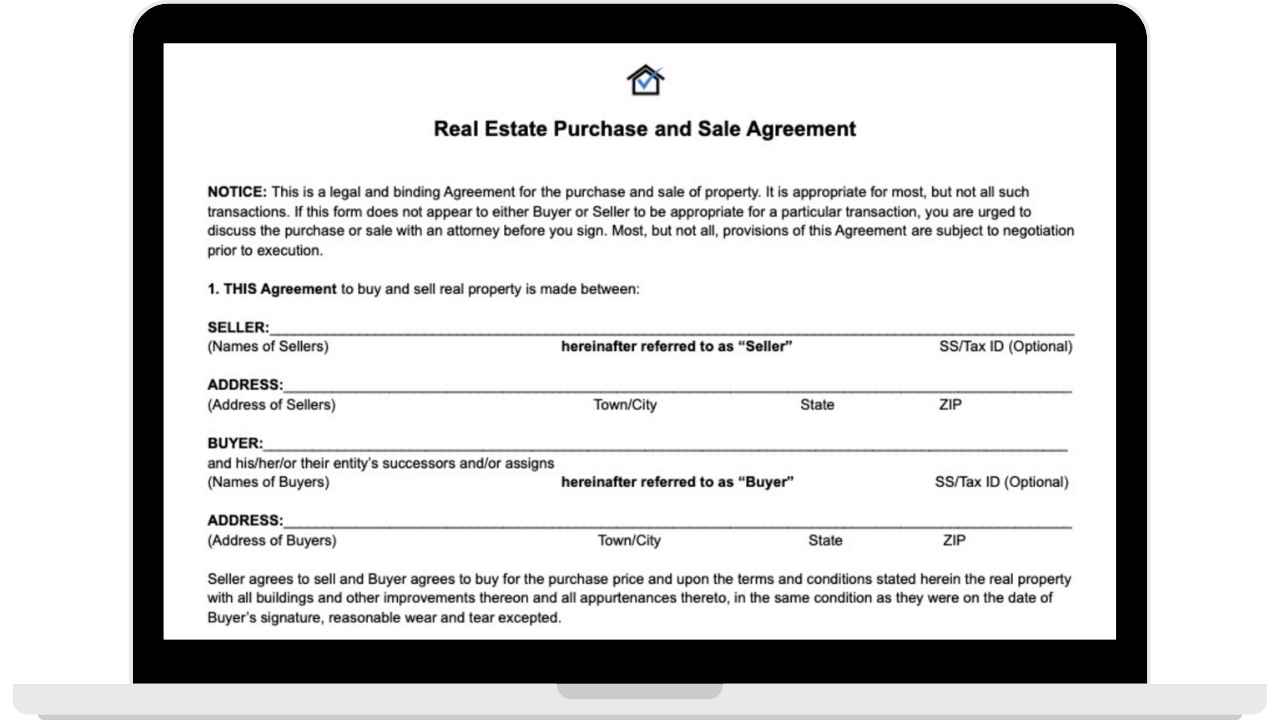

Section 1: Parties To The Agreement

This is where you name the seller and the buyer. Start with the seller, and pay attention here, because this is where most deals quietly die. There might be more than one seller: husband and wife, business partners, multiple heirs who just took title on an inherited property. Every owner on title has to be named and has to sign. If you're missing even one signature, the whole contract can be void. If you're not sure who actually owns it, call a title company and confirm before you write the offer.

Then the buyer — that's you, either your name as an individual or your LLC. Put your mailing address here, not the property address. People ask me all the time whether you need an LLC to wholesale. Short answer, no. But I'd do deals in an entity anyway; it protects you, and it looks more professional to a seller.

Right under the buyer line, you'll see language like "and his/her/their entities, successors, and/or assigns." That one line is what makes your contract assignable. All real estate contracts are assignable by default (with a few exceptions), but this makes it crystal clear that both parties agree to a potential assignment. If a seller ever asks about it, the honest answer is easy: you might close in a different LLC, you might bring in a money partner who funds the deal in their entity, you might fix-and-flip it or keep it as a rental. You haven't decided the exit yet; that's why it's there. It comes up rarely, and it's a normal, reasonable thing to say.

Section 2: Subject Property Information

This is the property you're buying: street address, city, county, state, zip. Get it exactly right; you do not want the wrong address on a purchase agreement. In 2C ("described as"), you note the type: single-family, multi-family, land. You'll also put the APN (the assessor's parcel number), which is basically the property's tax ID. Every property has one, and you can find it in seconds on the county tax site, the MLS, or Redfin.

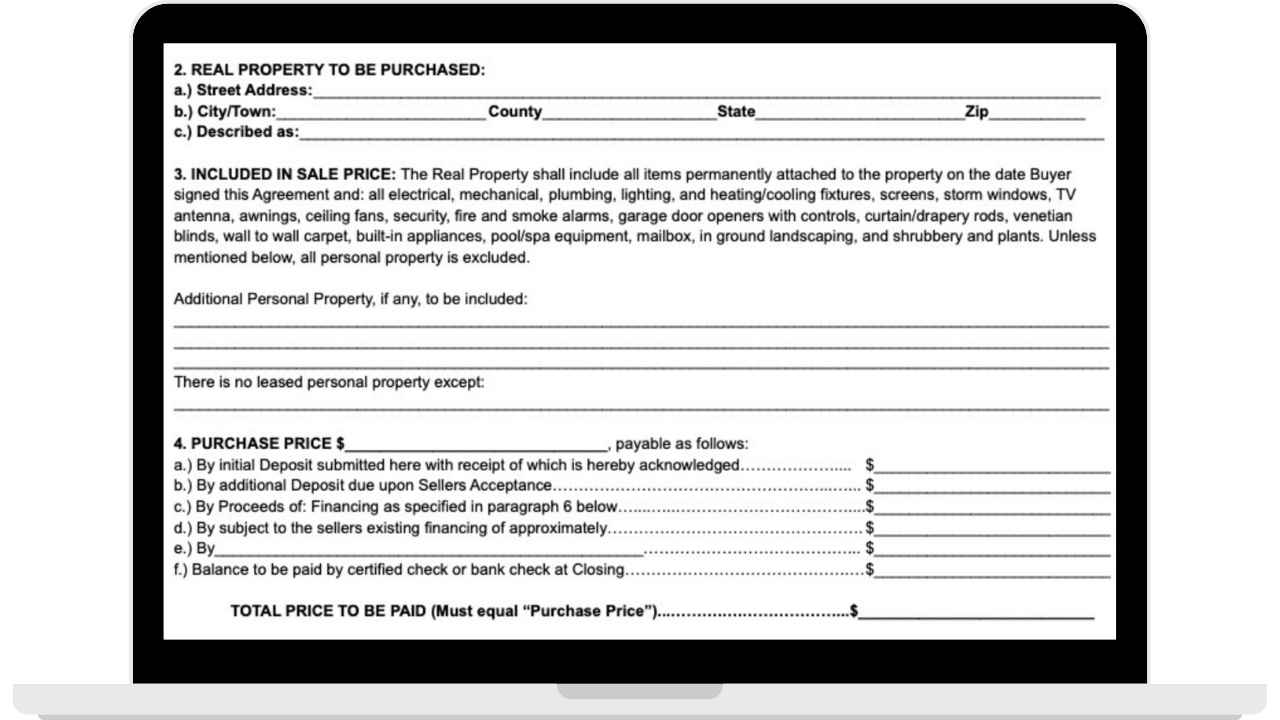

Section 3: Included In Sales Price

Everything permanently attached to the property conveys with the sale: the structure, flooring, built-in appliances, HVAC, fixtures, the pool and spa equipment, all of it. That's "real property." Personal property (furniture, a car, anything you can carry out) does not, unless you list it. There's a line for additional personal property, and you can get creative with it. Buying a place to Airbnb? Have it conveyed furnished. Seller's got a hoarder house full of stuff they don't want to deal with? You can agree to take possession of it and solve a real problem for them. It's a small section that can make a deal easier.

Section 4: Purchase Price

This is one of the most important sections. Put your total purchase price on the top line, and it has to match the total at the bottom. The lines in between just break down how that price gets paid:

- 4A / 4B — earnest money deposit. 4A is if you submit the deposit with the offer; 4B is if you submit it when the seller accepts. In most markets, it's 4B, and that's how I do it.

- 4C — financing. Leave it blank on a cash deal. If you were getting a loan, you'd put the loan amount here (e.g., $100,000 on a $200,000 property at 50%).

- 4D — subject-to. This is for taking over the seller's existing financing — a sub-to deal. Put the approximate loan balance here. Blank for a normal cash offer.

- 4E — cash. Write "CASH" here in big letters. It's a visual signal to the seller that this is a clean cash offer with no financing contingency, one of the biggest reasons sellers work with investors.

- 4F — balance. Anything left to reconcile so the lines add up to the full purchase price.

For the deposit amount, $500 to $1,000 works on a lower-priced deal, or use about 1% of the purchase price to make it competitive.

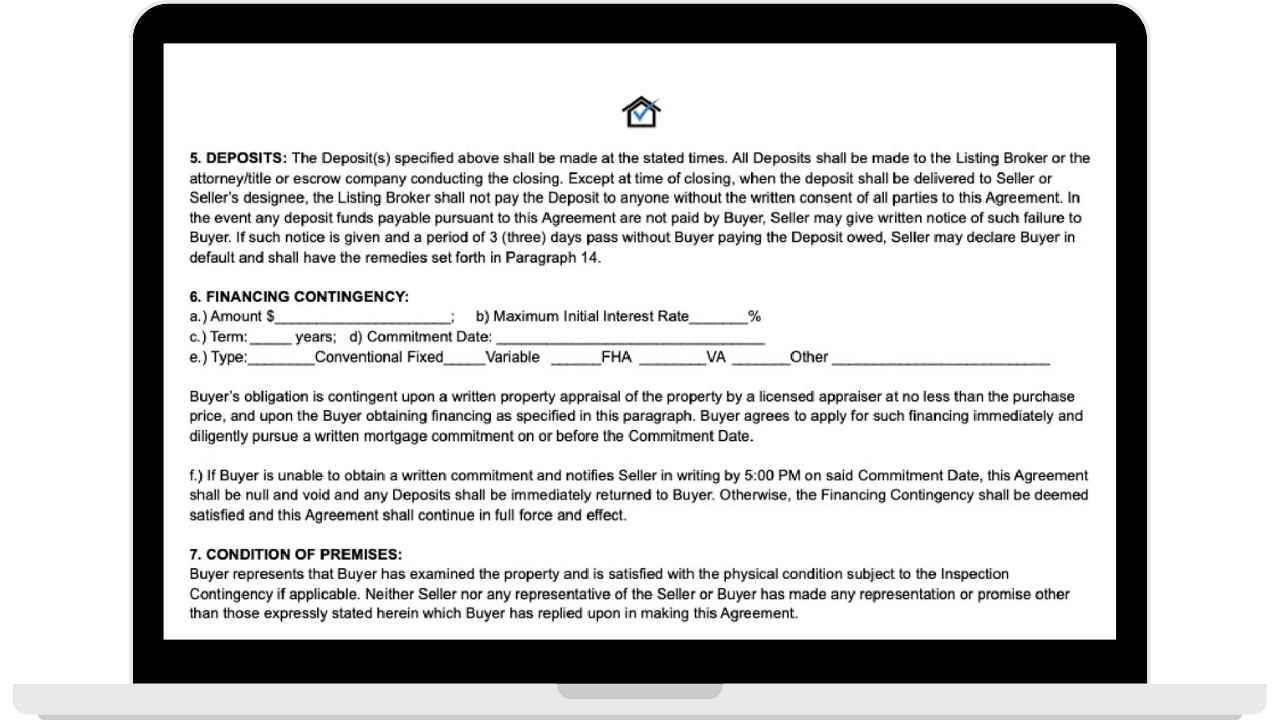

Section 5: Where The Earnest Money Goes

This just states that your earnest money does not go to the seller directly — it goes to a title company, escrow company, or closing attorney. You never hand a deposit straight to the seller; a neutral third party holds it. It also gives the seller a remedy if you don't submit your deposit: they can send you a notice, and if three days pass without it, they can cancel and treat you as in default. So don't tie up a contract and sit on your deposit.

How much earnest money? I like 1% to 3% of the purchase price. A bigger deposit makes a stronger offer because it shows commitment, but it also puts more of your money at risk, so as the buyer, you'd rather keep it lean. It's a negotiation. If you're unsure and the price is low, $1,000 or 1% is a safe place to land.

Section 6: Financing Contingency

Most wholesale offers are cash, so cross this section out — and use it as a selling point. No financing contingency means the seller doesn't have to worry about your loan falling through and killing the deal. If you did want a financing contingency, you'd list the loan amount, the maximum interest rate, the term, and a commitment date (when the contingency expires). There's usually also an appraisal piece — the property has to appraise at or above the purchase price, or you can terminate. But for a clean cash offer, this whole section comes out.

Section 7: Condition Of Premises

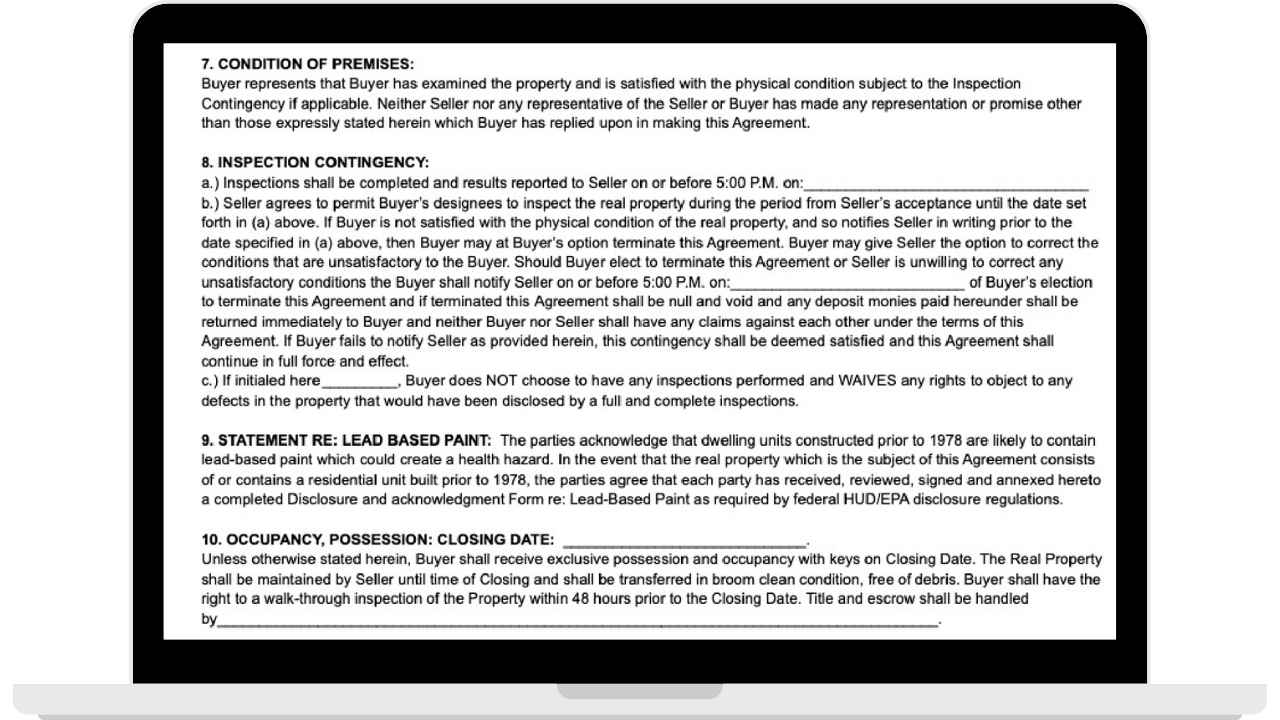

This is a short liability-release clause — it states you've examined the property and accept its physical condition, subject to your inspection contingency. It is not the inspection contingency itself. That's next, and it's the one that matters most.

Section 8: Inspection Contingency

The inspection contingency is your single most important protection as a wholesaler. It gives you a set window — usually 7 to 14 days — to inspect the property and, just as importantly, to get your cash buyers in and find your end buyer. Inside that window, your earnest money is refundable, and you can walk away.

This is the clause that protects your deposit, and it's the clause that makes wholesaling work. Two jobs at once: it lets you (or anyone you designate) inspect the property for real problems, and it's the window where you market the deal and get a cash buyer committed.

That "anyone you designate" part is worth underlining. The contract lets your designee do the inspection — a partner, a contractor, or your cash buyer themselves. That's how virtual and out-of-state deals work: you don't have to fly out, your buyer walks the property and gives you the green light. Honestly, as a wholesaler, I'd rather have the cash buyer walk it than pay for a formal home inspection — they're the ones deciding to buy, so let them set eyes on it and tell you it works.

The timeline (8A): I recommend 7 to 14 days. Whatever date the contract is signed, put a date 7–14 days out. Longer gives you more room to shop the deal and line up your buyer; shorter makes your offer stronger because it's more certain for the seller. It's a negotiation — at minimum I want about 5 days, but the more you can get, the better.

The pro move (8B): the contract also lets you notify the seller to either terminate or ask them to correct problems. This is your renegotiation lever. If your inspection turns up a foundation issue or framing damage the seller didn't disclose — or your cash buyers walk it and say the numbers only work $40k lower — you go back to the seller with a documented case for a price reduction. A lot of new wholesalers lock up a property too high just to "get something under contract." This is where you fix that. One thing you can't miss: you have to notify the seller of your decision by the date in the contract, or the contingency expires and your deposit is at risk. Mark that date.

Waiving it (8C): you can initial here to waive your inspection entirely. I wouldn't — not as a beginner, not unless you're 100% certain you're buying. It makes your offer stronger and your deposit non-refundable from day one, which is exactly the risk you don't want.

Section 9: Lead-Based Paint Disclosure

Standard disclosure for any property built before 1978. It's required on nearly every purchase agreement in the country. Nothing for you to do here — just know why it's there.

Section 10: Closing Date, Walkthrough & Title Company

This sets your closing date. I usually want at least a 14-day close — long enough to find the right cash buyer, short enough to stay competitive against financed offers that need 30 to 45 days. A cash close in two weeks is a real selling point with a motivated seller. Cater the date to what works for them.

This section also gives you a final walkthrough within 48 hours of closing — so you can confirm the property's in the same condition it was when you went under contract, no new fire, flood, or surprise damage. And it's where you name the title or escrow company. If you've got an investor-friendly one, put it here. If not, write "buyer's choice" so you keep the flexibility to pick later — often your cash buyer has a title company they prefer to use.

One thing that varies by market: who actually closes the deal. In California it's a title company plus an escrow company. In Illinois, deals are closed by attorneys. In Colorado it's a title company only. Before you do a deal somewhere new, find out who handles closings in that market and line up an investor-friendly title company or attorney ahead of time — not the week your deal is closing.

Sections 11 & 12: Warranty Deed & Clean Title

Section 11 says the title is conveyed by a warranty deed — the most favorable kind for you as the buyer. There are weaker deeds out there (a quitclaim, for example, doesn't guarantee clean title), and you don't want those. Section 12 is the one that does real work: the seller has to deliver a clean, marketable title at closing — no liens, no unpaid taxes, no creditor claims. If they can't, you can cancel and get your earnest money back.

This effectively acts as a title contingency. It matters most with distressed sellers, who sometimes have back taxes or liens they don't even know about. Your title company's search surfaces all of it, the seller clears it before closing, and you take the property free and clear — which is exactly what your cash buyer wants too.

Section 13: Prorations & Adjustments

This splits the ongoing costs and income — property taxes, water and sewer, insurance, and rents if it's tenant-occupied — down to the day of closing. The title company handles the math; you don't do anything here. If there are tenants, their security deposits transfer to the buyer too. It's just there to keep things fair between buyer and seller.

Section 14: Buyer Default & Liquidated Damages

The liquidated damages clause caps your financial risk at your earnest money deposit. If you default outside your contingencies, the most the seller can keep is your deposit — they can't come after you for more. Understand this clause and you can move with confidence, knowing exactly what your downside is.

This is the clause every real estate buyer should understand cold, no matter what contract you're using. Liquidated damages mean the financial ceiling on a buyer default is your deposit — and nothing beyond it. Put down $1,000, default outside your contingencies, and the seller's remedy is to keep that $1,000. Without this clause, a seller could theoretically come after you for a lot more. So this is your protection. It's also why staying inside your contingencies matters — that's what keeps your deposit refundable in the first place.

Section 15: Risk Of Loss Or Damage

If the property gets damaged while you're under contract — fire, flood, storm — this protects you. You can terminate and get your earnest money back, even if you'd already removed your inspection contingency. Or, if there's an insurance payout, you can choose to move forward and take the proceeds. Rare to need it, but it's real protection for you and your cash buyer if something happens before closing.

Sections 16–24: Standard Disclosures & Boilerplate

These are the standard clauses you'll see in most purchase agreements. A few worth naming:

- 16 — common interest community: applies if it's a condo or HOA; the seller delivers the HOA documents.

- 17 — listing broker: if an agent's involved, list them and check the box for dual agency if the listing agent represents both sides. If you're working directly with the seller, leave it blank.

- 18 — mandatory seller disclosures: varies by state; the seller has to provide whatever disclosures local law requires.

- 19 — equal housing: blanket fair-housing statement.

- 20 — addenda & advisories: attach anything extra here — a tenant rent roll, a trust disclosure, a short-sale addendum.

- 21 — additional terms: a blank space for anything unique to the deal. This is where you put creative terms that close a motivated seller — covering their moving costs, taking possession of items they're leaving behind, whatever solves their problem. Get an attorney's eyes on anything you add.

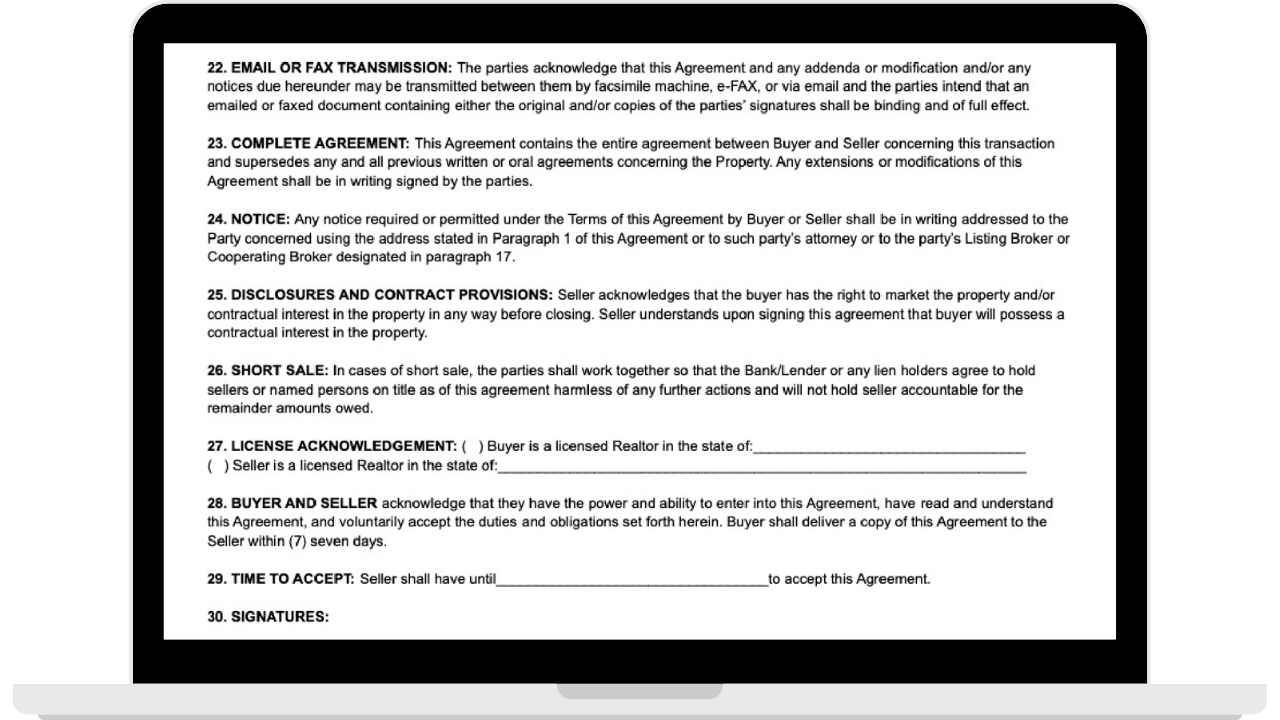

- 22–24 — communication & notices: email/fax counts as binding, this is the complete agreement, and notices have to be in writing.

Section 25: The Marketing Clause

Don't skip this one — it's the clause that makes the contract genuinely wholesaler-friendly. It states that the seller acknowledges you have the right to market the property and your contractual interest in it before closing. That's exactly what wholesalers do: go find a buyer for the deal. This clause puts it in writing that the seller understands and agrees to it. Make sure it's in your contract.

Sections 26–30: Short Sale, License, Deadline & Signatures

- 26 — short sale: cooperation language if the deal is a short sale.

- 27 — license acknowledgment: if you (or the seller) are a licensed agent or broker, you have to disclose it here. Check the box and note your state.

- 28 — capacity: both parties confirm they can enter the agreement and have read and understood it.

- 29 — time to accept: a deadline for the seller to accept your offer. This is a pro move — give them 24 to 72 hours. It turns up the heat and creates a little pressure so your offer isn't sitting open forever while they shop it around. You can always resubmit if it expires.

- 30 — signatures: get every seller's signature, sign yourself (with the right title if you're signing for an entity), and initial every page in the boxes at the bottom. Miss a signature and you don't have a deal.

Fill it out completely, get all the signatures, and you've got a legally binding agreement. Now you're ready to assign it.

How To Fill Out The Assignment Contract

The Assignment Contract transfers your rights as the buyer in the Purchase & Sale Agreement to a cash buyer in exchange for an assignment fee. You're the assignor, your buyer is the assignee. It's usually one page: match the original deal's details, name your fee, and both parties sign.

Once you've got a fully executed PSA, the Assignment Contract is how you actually get paid. It's short — usually a single page — and it does one thing: it swaps you out as the buyer and swaps your cash buyer in, for a fee. You don't sell the property. You sell your right to buy it. There's no assignment without a signed purchase agreement first — this is an addendum to that agreement, not a standalone deal.

Same note as above: the steps below show how an assignment contract typically works, for educational purposes — not legal advice. Assignment rules and what a contract can say vary by state, so have a licensed real estate attorney review your documents before you rely on them.

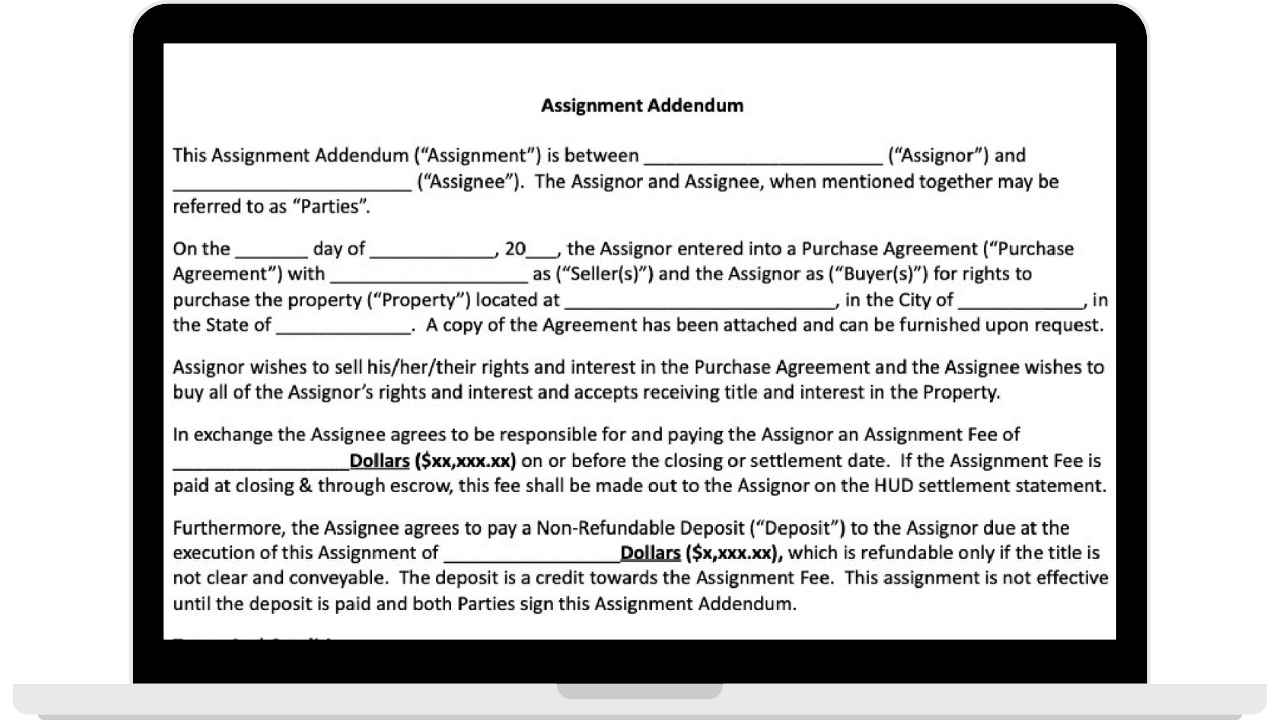

Step 1: Name The Parties (Assignor & Assignee)

You, the wholesaler, are the assignor — you're the buyer on the original contract. Your cash buyer is the assignee. Put your name or your LLC as the assignor and your end buyer as the assignee. That's it. Both can be individuals or companies — an LLC, a corporation, a trust.

Step 2: Match The Date, Seller & Property To The PSA

Everything here has to match your purchase agreement exactly. The date is the date the PSA was formed — usually the date of the last signature. Put the same seller name(s), the same property address (adding the APN never hurts), and your same buying entity as the assignor. If the seller, date, and address don't match the PSA, you've got a problem. Match them.

Step 3: Add Your Assignment Fee

This is your payday. Write the fee out in words first, then in numbers in parentheses — "Twenty Thousand Dollars ($20,000)" — so there's zero ambiguity about what you're owed. What you charge comes down to the deal: the better the discount you've got it under contract for, the more profit there is for the end buyer, the bigger the fee you can command. A clean deal might be $5,000 or $10,000; a great one can be far more.

Step 4: Set A Non-Refundable Deposit (Highly Recommended)

The non-refundable deposit is a portion of your assignment fee the buyer pays up front, when they sign — and it's a credit toward the total fee, not an extra charge. It's optional, but it's how you protect your money and get paid even if the buyer never closes.

This is optional, but I use it, and here's why it matters. The non-refundable deposit is money your cash buyer puts down at the moment they sign the assignment — and the contract isn't even effective until they pay it and both parties sign. It does two things. First, it makes the buyer commit financially, not just verbally. Second, it protects whatever you've already put into the deal.

Be clear on how it works: the deposit is a credit toward your total assignment fee, not money on top of it. Say your fee is $20,000 and you collect a $5,000 non-refundable deposit at signing — the buyer pays you $5,000 now and the remaining $15,000 at closing. Same total.

Now the protection play: size that deposit larger than whatever you've put into the deal. If you've got $2,000 of your own earnest money in escrow and you collect a $5,000 non-refundable deposit, then even if your buyer flakes and never closes, you keep the $5,000 — you're out your $2,000 EMD but still up $3,000. That's how you get paid even when a deal dies. The only time the deposit comes back to the buyer is if the seller can't deliver clean title — then everyone walks, and everyone's money is returned.

Step 5: Match The Closing Date & Sign

Put the same closing date as the PSA so the two contracts line up. The assignment language also holds you harmless if the buyer doesn't close, makes them responsible for closing, and gives you the right to reassign the deal to someone else (and keep their deposit) if they don't perform. Then both parties sign and date — your name or entity as assignor, your buyer as assignee. DocuSign or any e-signature tool is fine; that's how most virtual deals get done.

How You Actually Get Paid

Two ways, and you choose based on the deal:

- Through escrow (most common): put your fee on the assignment contract and send both contracts to the title company. Your fee becomes a line item on the settlement statement, and at closing, the title company wires it to you or cuts you a check. Bonus: being on the settlement statement builds a paper trail of closed deals — useful when you're newer and want to show lenders or partners you're actually doing this.

- Outside escrow: some wholesalers leave the fee off the assignment (or zero it out) and get paid directly by the buyer as a consulting or acquisition fee, so the seller and agents don't see the spread. Both are fine — it's about how you want to structure it.

One related question that comes up: when your buyer asks to review the original PSA before they commit — which they will — it's fine to black out your contract price on that copy if you don't want them seeing your spread. They're agreeing to the deal at the wholesale price; what you have it under contract for is your business. Just know that if you're getting paid through escrow, your fee shows on the settlement statement anyway. And closing costs don't come out of your fee — your assignment fee is a flat number paid on top of the sale price; the end buyer covers the closing costs as the actual buyer.

📓 From The Field

Ryan recently closed a virtual wholesale deal using this exact assignment contract and earned an $18,000 assignment fee — without ever visiting the property. He signed the PSA with the seller, signed the assignment with the cash buyer, sent both to the title company, and got paid by wire at closing. That's the whole model in one deal: two pieces of paper, no property visit, no renovation, paid at the closing table.

Once everything's signed, send both contracts to your title company or closing attorney and they take it from there. Your job is to keep everyone on the same page through closing. On closing day, your fee comes to you by wire or check — and that's the part that never gets old.

Secure Your Deal With Bulletproof Contracts

A weak contract is the fastest way to lose a deal — or your earnest money. The paperwork is what protects your spread, keeps the contract assignable, and gets you paid at the closing table. Download our attorney-drafted Wholesale Real Estate Contracts — the Purchase & Sale Agreement and the Assignment Contract — the same documents we use in our own deals and that thousands of our students have used to wholesale across the country.

Knowing what the contracts say is step one. Knowing how to actually use them to close a deal is where the money is. Our FREE Training shows you the whole process — finding the deal, locking it up with these exact contracts, and getting paid your assignment fee — the same system thousands of our students use.

You've got the contracts. This shows you how to put them to work on a real deal.

Key Wholesale Real Estate Contract Terms (Glossary)

Wholesale contracts come with their own vocabulary — assignor, assignee, equitable interest, liquidated damages, and more. Here's a plain-English glossary of the terms you'll see in a Purchase & Sale Agreement and an Assignment Contract, so nothing in the paperwork catches you off guard.

You'll run into these terms throughout both contracts. None of them are complicated once someone explains them in plain English — so here they are.

- Assignor

- You, the wholesaler. The assignor is the original buyer on the Purchase & Sale Agreement who assigns — transfers — their rights to someone else.

- Assignee

- Your end buyer — the cash buyer or investor who takes over your position in the contract and closes on the property.

- Assignment Fee

- Your profit. The fee the assignee pays you for the right to take over the deal — typically the spread between your contract price and theirs, commonly $5,000 to $20,000.

- Equitable Interest

- The legal interest you gain in a property the moment you sign a purchase agreement to buy it. It's what gives you the right to market and assign the deal — you're selling this interest, not the property itself.

- Equitable Conversion

- The legal principle that once a purchase contract is signed, the buyer holds equitable title to the property while the seller keeps legal title until closing. The doctrine of equitable conversion is what makes your equitable interest real and assignable.

- Earnest Money Deposit (EMD)

- A good-faith deposit you put down to show you're serious, held by a title or escrow company — not the seller. It's refundable while your contingencies are active and at risk if you default outside them.

- Contingency

- A condition that has to be met or you can walk away and keep your deposit. The inspection contingency is the wholesaler's most important one — it's your window to find a buyer and protects your earnest money.

- Liquidated Damages

- A clause that caps the financial penalty for a buyer default at the earnest money deposit. It means the most you can lose by walking away is your deposit — the seller can't sue you for more.

- Specific Performance

- A legal remedy where a court forces a party to complete the sale instead of just paying damages. It exists in most contracts, but attorneys will tell you it's rarely pursued — most sellers just keep the deposit and move on.

- Marketable Title

- Title that's free and clear of liens, back taxes, and other claims, so the seller can legally transfer ownership. If the seller can't deliver it, you can cancel and get your deposit back — it acts as a built-in title contingency.

- Double Close

- An alternative to assigning, where you actually buy the property and resell it — usually the same day — using two separate contracts instead of one assignment. More on this next.

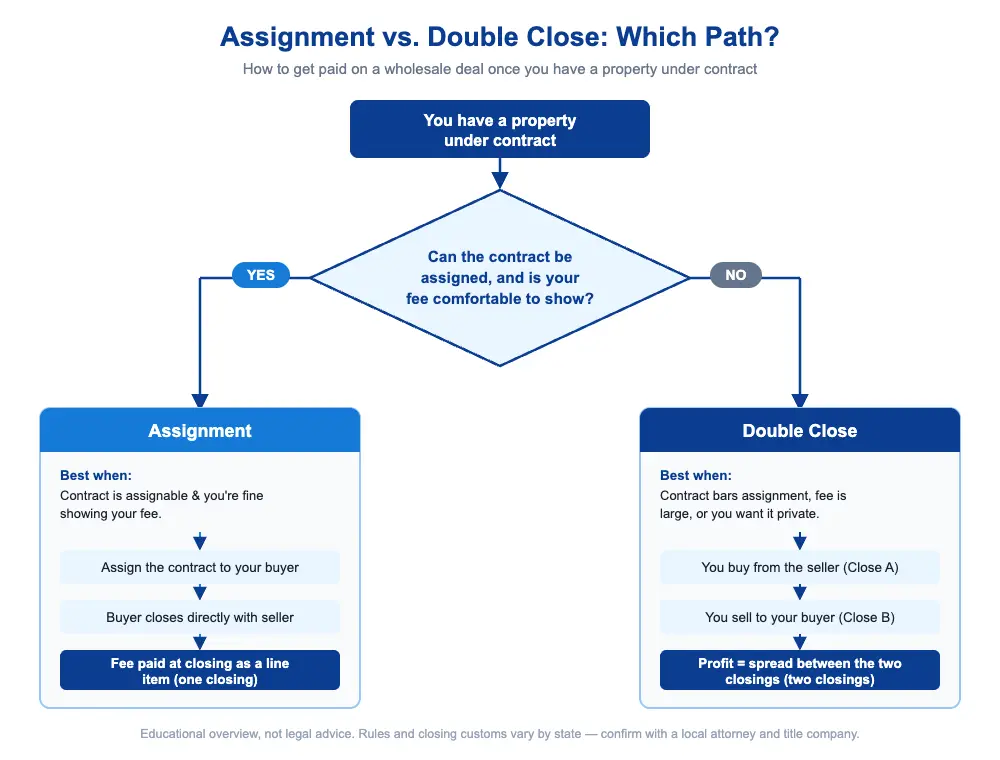

Assignment Contract vs. Double Close: Which Should You Use?

An assignment transfers your contract to a cash buyer for a fee and never puts the property in your name. A double close means you actually buy the property and resell it (usually the same day) using two contracts. Assignments are cheaper and simpler; double closes hide your profit and work when assigning isn't an option.

Assigning the contract is how most wholesale deals get done, and it's what I'd start with. But it's not the only way. The other main method is a double close, and there are specific situations where it's the smarter move. Here's how they stack up.

| Factor | Assignment Contract | Double Close |

|---|---|---|

| Do you take title? | No — never own the property | Yes — briefly, often the same day |

| Paperwork | One assignment contract | Two purchase agreements (A–B and B–C) |

| Closing costs | Little to none for you | Two sets of closing costs |

| Is your fee visible? | Yes — buyer sees it on the assignment | No — your spread stays private |

| Speed & simplicity | Faster, simpler — one closing | More moving parts — two closings |

| Best for | Most deals, beginners, smaller fees | Large spreads, privacy, non-assignable contracts |

How A Double Close Actually Works

A double close isn't an assignment at all; there's no assignment contract involved. Instead, you sign two purchase agreements:

- The A–B contract: between the seller (A) and you (B). This is you buying the property.

- The B–C contract: between you (B, now the seller) and your end buyer (C). This is you selling it.

You line up both closings to happen the same day, back to back. Here's the part that makes it work without your own cash: structured right, your end buyer's funds come into the title company first and are used to fund your purchase from the seller. So the money flows C → you → A, and your profit is the spread between the two prices.

Quick example: your A–B contract is $350,000, and your B–C contract is $400,000. Your buyer funds $400,000 (plus their closing costs) to the title company. The title company uses it to pay the original seller their $350,000, and the $50,000 difference — minus closing costs — gets wired to you. We've done double closes without putting up a dollar of our own money this way. It's possible — but it depends on structuring it correctly and using a title company that does this kind of transaction, so confirm that up front.

When To Double Close Instead Of Assign

Three situations where a double close is the better call:

- You don't want to show a big fee. If you've got a deal where you can charge a $50,000 or $100,000 spread, putting that on an assignment contract can spook the buyer — they see the number and push back. A double close keeps your profit private; the buyer only sees the price you're selling at.

- The contract can't be assigned. If a contract genuinely prohibits assignment, or a bank or seller won't allow it and you don't want to amend, you can double close instead — you're buying and reselling, not assigning, so the restriction doesn't apply.

- You're avoiding a tax or transfer issue. Some states withhold a percentage of sale proceeds from out-of-state sellers, and that can hit a double close. See the field note below — sometimes assigning is simply cleaner.

The tradeoff is always closing costs. Because you're both a buyer and a seller, you pay two sets of closing costs — transfer taxes, title fees, escrow, recording — which eat into your profit. That's why double closing makes the most sense when the spread is big enough (usually $20,000–$30,000+) to absorb those costs comfortably. On a smaller fee, assign it.

📓 From The Field

On an out-of-state deal in Colorado, our team planned to double close — until the title company flagged that the state would withhold about 2% of the sale price from the proceeds (roughly $9,000–$10,000 on a $460,000 sale) because we were an out-of-state company. That money gets held until you file taxes there and claim a refund. So instead of tying it up, we restructured the deal as an assignment and sidestepped the withholding entirely. The lesson: if you're wholesaling at a distance, ask your title company about out-of-state withholding before you decide how to close. It varies by state — this isn't tax advice, just a reason to ask the question early.

Bottom line: assign when you can, double close when you should. Most deals are clean assignments. Reach for the double close when the spread is large, the profit needs to stay private, or assigning isn't on the table.

Is A Wholesale Real Estate Contract Legal?

Yes. Wholesaling real estate with contracts is legal in all 50 states, and contracts are assignable by default. A handful of states regulate how you wholesale — requiring disclosure or limiting how you market — but none ban it outright. The key is following your state's rules and using a contract that establishes your equitable interest.

Let's clear this up, because it's the question that keeps people from ever starting. Wholesaling is legal. Assigning a real estate contract is legal. As a matter of contract law, purchase agreements are assignable by default in every state unless the contract itself says otherwise — a principle reflected in the Restatement (Second) of Contracts § 317, which holds that contractual rights are assignable unless the contract precludes it. What you're selling is your equitable interest in the deal — a real, recognized legal interest you hold the moment you sign the purchase agreement.

Here's the honest, current picture as of 2026: no state has outright banned wholesaling. What's changed in recent years is that some states have added regulation around it — mostly disclosure requirements (telling the seller you're a wholesaler who intends to assign) and limits on marketing a property you don't own. That's not a ban; it's a set of rules to follow. The wholesalers who get in trouble are the ones who ignore disclosure and act like they own a property they don't.

How To Wholesale Real Estate Legally In ANY State (+FREE CONTRACTS)!

Ryan Zomorodi breaks down how to wholesale legally in any state — including three attorney-reviewed strategies for closing deals even when a contract can't be assigned.

What If The Contract Can't Be Assigned?

This is the situation people panic about, and they shouldn't. First, the premise is usually wrong: most contracts — including the majority of Realtor contracts, like the TREC contract in Texas and the Florida Realtor contract — are assignable. Some, like the California Residential Purchase Agreement, contain language that says you can't assign without the seller's written consent, "which shall not be unreasonably withheld." That's not a wall; it's a step. And even a contract that flatly prohibits assignment can be worked around. You've got three attorney-reviewed strategies.

1. Amend The Contract

The simplest fix. Any contract can be amended if all parties agree — that happens in nearly every real estate transaction. So you get the seller, you, and your buyer to sign an amendment that lets you close in a different entity. This is the single most useful thing to understand about contracts: everything in them is negotiable. You can change the closing date, the price, the entity — anything — as long as everyone agrees. A "non-assignable" contract is just one amendment away from being assignable.

How you have that conversation matters more than the contract language. Don't say: "Hey, I'm wholesaling this to some buyer I found online, please sign off so I can collect my fee." Instead: "We're excited to move forward on this. My partner is bringing the capital, so we've decided to close in their LLC — could you sign this addendum so we can update the name and forward it to title?" Same outcome, completely different reception. It's professional, it's true, and it's how deals actually get amended.

2. Sell The LLC (LLC Assignment)

Put the property under contract in a fresh LLC — a single-purpose entity — instead of your personal name. Then, rather than assigning the contract, you sell the membership interest in the LLC to your buyer. The buyer on the contract never changes; you're selling the company that holds the contract. Nothing is "assigned," nothing is marketed, so it sidesteps assignment restrictions and most state wholesaling rules entirely — there's no law against selling an LLC.

Here's the math on a real one: say you've got a property under contract in a fresh LLC for $150,000. Instead of assigning, you sell the membership interest in that LLC to your buyer for $180,000 — they step into the company that holds the contract, and your $30,000 is the spread. Nothing was assigned, and nothing was marketed; you sold a business that happened to own a purchase contract.

The practical part: an attorney can spin up a single-purpose LLC in 24–48 hours, usually for around $300 in state filing fees plus a small attorney fee. It doesn't even need an EIN or a bank account — it's a clean shell whose only asset is the purchase contract. And assigning a contract to your own wholly-owned LLC is never an issue, even on a non-assignable contract, because it's still you.

3. Use A Land Contract Or Joint Venture

Two more tools your attorney can structure: a land contract (a seller-financing arrangement that changes how the transfer works), or a joint venture agreement with your end buyer, where you partner on the deal and split the profit rather than assigning. These are more situational, but they're legitimate ways to get a deal closed when a straight assignment isn't the right fit. Run them by a local attorney.

A Note On State Rules: Texas As An Example

State requirements change, and Texas is a good example of how. As of recent updates to the Texas Property Code and Occupations Code (effective September 2024), a wholesaler in Texas has to give written notice to both the seller and any buyer disclosing that they hold an equitable interest — not legal title — in the property before the deal goes through. Contracts there remain assignable by default. It's not a ban; it's a disclosure rule. And it's exactly the kind of thing that varies from state to state and can change year to year.

So the move is simple: before you wholesale in a given state, know that state's current disclosure and marketing rules, use a contract built for wholesaling, and have a local real estate attorney review your approach. Texas is just one example — here are a few more states that have added their own rules recently.

📍 Check Your State's Rules First

A handful of states have added new rules in 2025–2026. This is current as of 2026 and changes fast, so confirm your state's requirements before you sign anything:

- North Carolina — House Bill 797 (effective Oct 1, 2025) now treats residential wholesaling as brokerage activity requiring a real estate license, and gives sellers a 30-day right to cancel.

- Oklahoma — the Predatory Real Estate Wholesaler Prohibition Act, strengthened by SB 1075 (effective Nov 1, 2025), requires a license to publicly market a deal and now includes double closing in its definition of wholesaling.

- Illinois — limits unlicensed wholesalers to one deal per 12-month period under the Real Estate License Act.

- Ohio — SB 155 requires a bold-faced disclosure before the contract is signed; failure to provide it gives the seller unconditional cancellation rights.

- Maryland & Connecticut — both added new disclosure and registration requirements in 2025–2026.

For a full state-by-state breakdown, see our guide on whether wholesaling is legal in your state.

Read Also: Is Wholesaling Real Estate Legal In Texas?

This section explains general practices, not legal advice. Wholesaling laws vary by state and change over time — always confirm current requirements with a licensed real estate attorney in your market before doing a deal.

Do You Need A License To Write A Wholesale Real Estate Contract?

No. You do not need a real estate license to write or use a wholesale real estate contract. You're acting as a principal buyer in your own deal, not representing someone else's transaction. A few states have tightened rules around how often you can wholesale, so check your local requirements.

You don't need a license to wholesale. When you sign a purchase agreement to buy a property, you're a principal in the deal — the buyer — not an agent representing someone else. Writing your own offer and assigning your own contract doesn't require a license anywhere.

The line to watch is the one between investing and brokering. A license is for representing other people's transactions for a commission. Wholesaling is buying and selling your own contractual interest. That said, a handful of states have added rules about how frequently you can do this before it starts to look like unlicensed brokerage, so know your state's current stance. And being licensed isn't a disadvantage — plenty of wholesalers, myself included, hold a license because it gives you MLS access and more deal flow. It's just not required.

Wholesale Real Estate Contract Template (Free PDF)

A wholesale real estate contract template gives you a ready-made Purchase & Sale Agreement and Assignment Contract you can fill in for your own deals. Below is a simplified look at what a wholesale contract contains, plus a free, attorney-drafted PDF you can download and use.

Here's a simplified look at the structure of a wholesale contract, so you can see how the pieces fit together before you download the full versions. This is an educational sample — not a complete legal document — meant to show you the bones of the agreement.

REAL ESTATE PURCHASE & SALE AGREEMENT

(Simplified sample layout)

ASSIGNMENT OF CONTRACT

(Simplified sample layout)

This is a simplified educational sample, not a legal document. Always use a complete, attorney-reviewed contract for actual deals and confirm it meets your state's requirements.

Download The Full Wholesale Contracts (Free PDF)

Get the complete, attorney-drafted versions of both contracts — the Purchase & Sale Agreement and the Assignment Contract — ready to fill in and use on your next deal. These are the same documents we walked through above and use in our own business.

Advantages Of Using A Wholesale Real Estate Contract

A wholesale contract lets you profit from real estate with little money, no ownership, and limited risk. You can start with almost nothing out of pocket, get paid fast at closing, and avoid the costs of renovations, financing, and property management entirely.

Wholesaling is one of the lowest-barrier ways into real estate, and the contract is what makes that possible. Here's why:

- Little to no money out of pocket. There are no fees to assign a contract, and, structured right, your end buyer can even fund the earnest money. You can do a deal without putting up much of your own cash.

- You get paid fast. Wholesalers get paid at closing — often within weeks of going under contract. Compare that to a flip (months) or a rental (years to see real returns).

- It builds a track record you can show. When you get paid through escrow, your fee shows up as a line item on the settlement statement — and that paper trail is worth more than it looks when you're newer. A stack of closing statements is how you prove to private lenders, partners, and bigger buyers that you actually close deals, not just talk about them. It's the difference between saying you wholesale and showing it.

- No renovations, tenants, or loans. You never own the property, so you skip the contractors, the tenant headaches, and the financing risk. Ask anyone who's managed a rehab — that's a real advantage.

- Low risk, defined downside. With a solid contract, your worst case is usually capped at your earnest money deposit thanks to the liquidated damages clause. You know your downside going in.

- It's the best place to learn. Wholesaling teaches you to find deals, analyze them, and talk to sellers and buyers — the core skills behind every other real estate strategy. It's how thousands of investors close their first deal.

It's not without tradeoffs — you leave the bigger long-term profits of flipping and holding on the table, your fee is taxed as ordinary income, and you're only as strong as your cash buyers. But as a way to start making money in real estate with limited capital and limited risk, it's hard to beat. The contract is the tool that makes all of it work.

Wholesale Real Estate Contract FAQs

Final Thoughts On Wholesale Real Estate Contracts

Wholesaling comes down to two pieces of paper: the Purchase & Sale Agreement that locks up the deal, and the Assignment Contract that gets you paid. Understand what every clause does, and you stop guessing — you know exactly what protects you, what your downside is, and how the money reaches your account.

That confidence is the whole point. The wholesalers who make it aren't the ones with the most money or the best market. They're the ones who know their contracts cold, so when a deal gets tight — the inspection clock is running, a buyer wavers, a seller gets nervous — they know precisely where they stand and what move to make next. The ones who panic are almost always the ones who never read the contract.

And not every deal closes. A buyer flakes, a seller gets cold feet, a title issue surfaces. That's normal. A strong contract means those moments cost you little or nothing — your deposit is protected, your downside is capped, and you move to the next one. Download the free contracts, study them until they're second nature, and put them to work. That's how first deals turn into a business.

Most people read about wholesaling, download the contracts, and never do a deal. The ones who close are the ones who follow a proven process from day one instead of guessing their way through it.

Our FREE Training walks you through exactly how to find deals, use these contracts to lock them up, and build real income — without spending a dollar on marketing or learning the hard way. Watch it today, then go put it to work.

About The Author

Founder & CEO, Real Estate Skills

Alex Martinez is the Founder and CEO of Real Estate Skills. With more than a decade of investing experience and 33+ residential properties acquired, he has personally wholesaled and flipped houses across the country. Through Real Estate Skills, Alex and his team have helped thousands of students learn how to find deals, use the right contracts, and close profitable real estate transactions.

Real Estate Skills is not a law firm, and the information in this article is provided for educational purposes only — it does not constitute legal, tax, or financial advice. Wholesale real estate laws and contract requirements vary by state and change over time. Real estate investing carries risk, and past results do not guarantee future outcomes. Always consult a licensed real estate attorney and your own tax and financial advisors before entering into any contract or transaction.

👉FREE Training

How To Consistently Wholesale, Flip Houses, & Invest In Rental Properties From The MLS

(Without Spending $1 On Marketing)

Alex Martinez, the founder of Real Estate Skills, is known for his strong, practical expertise in real estate, starting from a beginner with no family connections in the industry to completing over 50 real estate deals, including wholesale and flips, within his first year.

He has dedicated his career to providing cutting-edge education and resources for real estate professionals. He emphasizes the importance of self-taught knowledge through mentors, books, and hands-on experience.

His journey from earning a modest income to becoming a successful real estate entrepreneur and educator showcases his expertise and dedication to the field.

Ryan Zomorodi, co-founder and COO of Real Estate Skills, leverages his experience from a diverse background in real estate investment, construction management, and entrepreneurship to provide comprehensive education in the real estate sector.

His expertise is rooted in hands-on experience, extensive industry knowledge, and a commitment to empowering others through education.

Ryan's journey reflects a blend of practical experience and entrepreneurial success, contributing to his role in developing a platform that educates and supports aspiring real estate professionals.

Read Ryan's Full Bio >>