What Is Seller Financing in Real Estate & How Does It Work?

Aug 22, 2025

Buying and selling real estate does not always require a traditional bank loan. Seller financing (also called owner financing) is a creative option where the seller acts as the lender, allowing the buyer to make payments directly instead of going through a bank.

This flexible strategy can help buyers who do not qualify for conventional mortgages, while also offering sellers the chance to earn interest income and close deals faster.

Quick Summary: Seller Financing

- Definition: Seller financing (owner financing) is when the property seller acts as the lender, letting the buyer pay them directly instead of using a bank.

- Who it’s for: Buyers who can’t qualify for traditional loans, investors seeking flexible terms, and sellers wanting more buyers or interest income.

- How it works: Buyer pays a down payment, signs a promissory note, then makes monthly installments. Many deals include a balloon payment after a few years.

- Pros for buyers: Easier qualification, faster closing, lower closing costs, flexible terms.

- Cons for buyers: Higher rates, balloon payments, limited availability, credit not always reported.

- Pros for sellers: Steady income, higher sale price potential, faster sale.

- Cons for sellers: Risk of default, delayed full payment, legal requirements.

According to Zillow's 2024 survey, 35% of recent successful buyers secured a low rate through special financing from the seller or builder. That survey also showed "nearly half of recent successful buyers were able to secure a rate below 5%."

In this guide, we explain what seller financing is, how it works, and the pros and cons for both buyers and sellers. You will also learn about the different types of seller-financed agreements, the legal considerations you should know, and real-world examples that show how these deals are structured.

By the end of this article, you will know exactly how seller financing works, who it benefits, and whether it is the right approach for your next real estate deal.

- What Is Seller Financing?

- What Is Seller Financing Real Estate?

- Seller Financing Example In Real Estate

- How Does Seller Financing Work?

- Types Of Seller Financing Agreements

- How To Find Seller Financing Homes For Sale

- How To Structure A Seller Financing Deal

- Pros of Seller Financing

- Cons of Seller Financing

- Seller Financing FAQs

What Is Seller Financing?

Seller financing, also called owner financing or a purchase-money mortgage, is an agreement where the seller of a property provides financing directly to the buyer. Instead of using a traditional bank loan, the buyer makes payments to the seller based on agreed terms outlined in a promissory note.

In this setup, the seller essentially acts as the bank, earning interest on the loan while helping the buyer purchase the property.

While seller financing can be used for other high-value assets like automobiles or art, it is especially common in real estate transactions, where buyers may not qualify for conventional financing or prefer a faster, more flexible deal structure.

This FREE Training gives you the same system our students use to start fast and scale smart. Watch it today—so you can stop wondering and start closing.

What Is Seller Financing In Real Estate?

In real estate, seller financing allows buyers to purchase a home or investment property without relying on a mortgage lender. The seller covers the purchase price of the property, minus any down payment from the buyer, and the buyer makes monthly payments directly to the seller.

The terms of the arrangement, including purchase price, interest rate, repayment schedule, and any balloon payment, are set in a promissory note. Typically, the seller keeps the property title until the buyer has completed all payments or refinanced with a traditional mortgage.

This structure allows buyers who might not qualify for a bank loan to purchase a home still, and it allows sellers to attract more buyers, earn a steady income, and potentially achieve a higher sale price

How Does Seller Financing Work?

Seller financing works much like a traditional mortgage, but instead of borrowing from a bank, the buyer borrows directly from the seller. The seller agrees to finance the purchase price of the property (minus any down payment), and the buyer makes monthly payments according to the agreed terms.

- Purchase price

- Interest rate

- Repayment schedule

- Balloon payment (if any)

- Consequences of default

In many states, the agreement is secured by a mortgage or deed of trust that is recorded with the local authority. Once the deal is finalized, the buyer takes possession of the property and begins making payments.

Most seller financing agreements are short-term. Although payments may be structured on a 30-year amortization, they usually include a balloon payment due within 3–5 years. The expectation is that the buyer will refinance with a traditional lender or pay off the remaining balance at that point.

To qualify, sellers typically must own the property free and clear of a mortgage. If there is still an outstanding loan, the seller’s lender must approve the arrangement. While this is less common, exceptions do exist.

Seller Financing Example In Real Estate

Imagine a buyer wants to purchase a $150,000 home but is denied a conventional loan because their debt-to-income ratio is too high. The buyer has saved a large down payment of $95,000, so they approach the seller about a seller financing arrangement.

The seller agrees. Instead of going through a bank, the buyer pays the seller directly:

- Purchase price: $150,000

- Down payment: $95,000

- Financed amount: $55,000

- Interest rate: 7%

- Term: 5 years, amortized over 20 years

- Monthly payment: about $426

- Balloon payment: about $47,000 due at the end of year 5

The buyer also covers property taxes and insurance. At closing, the buyer receives the title, though the seller retains a lien until the full balance is paid or refinanced.

This example shows how seller financing can help a buyer who cannot qualify for a traditional mortgage while giving the seller a steady monthly income plus a balloon payoff.

Read Also: Private Money Lenders: The (ULTIMATE) Guide

Types Of Seller Financing Agreements

Seller financing can be structured in several different ways. Each option has unique rules, risks, and benefits for buyers and sellers.

Here are the most common types:

- All-Inclusive Mortgage (Wraparound Mortgage): The seller finances the property while still keeping their original mortgage in place. The buyer makes one payment to the seller, who continues paying their existing loan.

- Pros: One monthly payment for the buyer, seller may profit from the interest rate spread.

- Cons: Seller remains responsible for the original loan; due-on-sale clause can trigger foreclosure if lender objects.

- Junior Mortgage (Second Mortgage): If the buyer secures a traditional loan but it does not cover the full purchase price, the seller may provide a smaller second loan to make up the difference.

- Pros: Helps buyers close deals with less upfront cash; gives sellers interest income.

- Cons: Higher risk for the seller if buyer defaults; second lien is subordinate to the primary lender.

- Holding Mortgage: The seller extends credit directly to the buyer with a promissory note and mortgage, acting as the bank. This is the classic version of seller financing.

- Pros: Simple, direct arrangement; flexible terms for both parties.

- Cons: Seller assumes full risk of buyer default; limited liquidity until payoff.

- Land Contract (Contract for Deed): The buyer makes installment payments, but the seller keeps legal title until the final payment is made. The buyer holds “equitable title” during the contract term.

- Pros: Easier qualification for buyers; seller keeps control until fully paid.

- Cons: Buyers risk losing equity if they default; title transfer delayed until final payoff.

- Lease Option (Rent-to-Own): The buyer rents the property for a set time with the option to purchase later. A portion of rent may count toward the purchase price.

- Pros: Low upfront cost; lets buyer “test” the property before purchase.

- Cons: If buyer does not buy, they lose rent credits; seller must maintain the property until purchase.

- Assumable Mortgage: Instead of creating a new loan, the buyer takes over the seller’s existing mortgage with lender approval. FHA, VA, and some adjustable-rate mortgages are assumable.

- Pros: Buyer may secure lower interest rates; smoother transaction if approved.

- Cons: Requires lender approval; seller’s liability may continue unless formally released.

How To Find Seller Financing Homes For Sale

While seller financing is growing in popularity, most home listings will not openly advertise that the seller is willing to finance the purchase. Many homeowners do not even know what owner financing is, which means buyers need to be proactive and creative in their search.

Here are the best ways to find homes with seller financing:

- Use Specialized Listing Websites: Platforms like Zillow and Redfin often let you filter or search for “owner financing” or “seller financing” in property descriptions. Look closely at listing notes and keywords.

- Work with a Local Real Estate Agent: An experienced agent who knows your market can uncover off-market opportunities and identify sellers who may be open to financing, even if it is not advertised

- Check Public MLS Access: In some counties, the Multiple Listing Service (MLS) is open for public browsing. Search listing comments for phrases like “owner will carry,” “seller financing available,” or “contract for deed."

- Look for For Sale By Owner (FSBO) Listings: FSBO sellers are often more flexible and may consider creative options like seller financing. Watch for yard signs or FSBO sections on major real estate websites.

- Contact Rental Property Owners: Landlords with vacant or long-term rentals may be open to a lease option or rent-to-own arrangement instead of continuing to rent.

- Ask the Seller Directly: Many sellers simply have not considered owner financing. If you are interested in a property, it never hurts to ask whether they would consider financing the sale.

Read Also: How To Get MLS Access: The (Ultimate) Guide

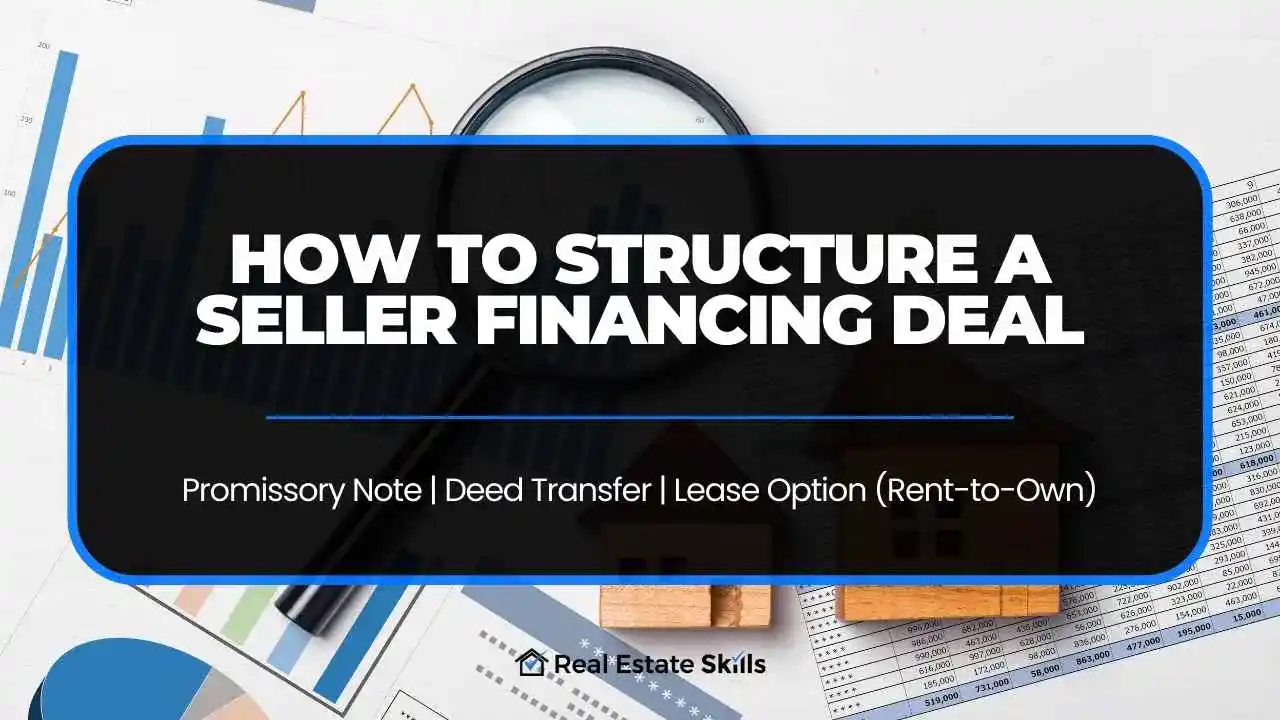

How To Structure A Seller Financing Deal

Like any real estate transaction, a seller-financed agreement must be supported by clear underwriting and legal documentation. The exact structure depends on what both the buyer and seller want, but there are three common ways to arrange these deals:

-

Promissory Note with Mortgage or Deed of Trust

-

The buyer signs a promissory note outlining the purchase price, interest rate, repayment schedule, and default terms.

-

The note is secured by the property as collateral through a mortgage or deed of trust.

-

The buyer's name goes on the title, and the agreement is recorded with the local county.

-

-

Deed Transfer upon Final Payment (Land Contract / Contract for Deed)

-

The seller keeps legal title until the buyer finishes making all required payments.

-

Once the balance is paid (or refinanced with a traditional loan), the deed transfers to the buyer.

-

This structure protects the seller but delays the buyer’s full ownership until payoff.

-

- Lease Option (Rent-to-Own)

-

The buyer rents the property for a set period while making monthly payments.

-

A portion of rent may be applied toward the purchase price.

-

At the end of the lease, the buyer has the option to purchase the property, usually with a balloon payment or refinancing.

-

No matter which structure you choose, professional guidance is critical. A qualified real estate attorney can draft the promissory note, record the deed, and ensure that both parties are protected under state and federal law.

Pros of Seller Financing

Seller financing can be a smart strategy when used in the right circumstances. Both buyers and sellers can benefit from the flexibility, speed, and financial advantages that come with skipping the traditional bank loan process.

Advantages for Sellers

- Sell “as-is”: No need to make costly repairs or meet strict lender requirements.

- Steady cash flow: Collect monthly payments with interest, often earning a higher return than an immediate lump-sum sale.

- Attract more buyers: Reach buyers who do not qualify for conventional loans, expanding the potential pool of purchasers.

- Faster closings: Avoid lender delays and close on your timeline.

- Added security: Retain title until the loan is fully paid, and reclaim the property if the buyer defaults.

- Potential tax benefits: Spread out capital gains over time through installment sales.

Advantages for Buyers

- Easier qualification: Credit score or income issues may not block approval if the seller is flexible.

- More purchasing power: Buyers may be able to afford homes above what banks would approve.

- Lower upfront costs: Reduced bank fees, closing costs, and sometimes smaller down payments.

- Faster, simpler process: No lengthy underwriting or mortgage approvals.

- Option to “test” before buying: Lease option arrangements let buyers live in the home while building toward ownership.

Cons of Seller Financing

Seller financing offers flexibility, but it also comes with risks and limitations for both buyers and sellers. Understanding the drawbacks is just as important as knowing the benefits.

Disadvantages for Buyers

- Higher interest rates: Sellers often charge more to offset their risk.

- Balloon payments: Many deals require a large lump-sum payoff within 3–5 years.

- Limited availability: Not all sellers are willing or able to offer financing.

- Credit concerns: Buyers with very poor credit may still be turned down if the seller sees them as too risky.

- Due-on-sale clauses: If the seller has an existing mortgage with this clause, their lender may block the financing arrangement.

Disadvantages for Sellers

- Risk of default: If the buyer stops paying, the seller must foreclose or take the property back.

- Property responsibilities: Until the note is fully paid, the seller may still have to handle upkeep or liabilities in the event of default.

- Legal restrictions: Federal and state laws can limit balloon payments, require disclosures, or mandate using a licensed mortgage loan originator.

- Delayed payout: Sellers give up an immediate lump-sum sale and must wait years for full payment.

Frequently Asked Questions About Seller Financing

Still have questions about seller financing? This FAQ covers the key details buyers and sellers want to know, from how deals are structured to the pros, cons, and legal requirements.

1. What is seller financing in real estate?

Seller financing, also called owner financing, is when the property seller provides financing directly to the buyer instead of requiring a bank mortgage. The buyer makes payments to the seller according to agreed terms, usually outlined in a promissory note.

2. How does seller financing work?

The buyer typically pays a down payment, then makes monthly installments with interest directly to the seller. Many agreements include a balloon payment after a few years, at which point the buyer refinances or pays off the balance.

3. Is seller financing a good idea for buyers?

It can be, especially for buyers who cannot qualify for a conventional loan, need flexible terms, or want to close quickly. The tradeoffs may include higher interest rates and a required balloon payment.

4. Is seller financing a good idea for sellers?

Yes in many cases. Sellers may attract more buyers, sell faster, and earn interest income. They also take on default risk and must ensure compliance with state and federal law.

5. What are the risks of seller financing?

For buyers: higher rates, large balloon payments, and fewer protections than traditional mortgages. For sellers: default risk, delayed full payout, and potential legal restrictions such as due-on-sale clauses or loan originator requirements.

6. What types of seller financing exist?

Common options include a promissory note with a mortgage or deed of trust, land contract (contract for deed), lease option (rent to own), all-inclusive or wraparound mortgages, junior mortgages, and assumable mortgages.

7. Do sellers need to own their home outright to offer financing?

Usually yes. If there is an existing mortgage, the seller often needs lender approval, especially if the loan includes a due-on-sale clause.

8. Where can I find seller financing homes for sale?

Search for keywords like “owner financing” or “seller will carry” on sites such as Zillow and Redfin. Check public MLS portals, FSBO listings, contact rental property owners, or ask sellers directly.

9. Does seller financing affect a buyer’s credit?

Not always. If payments are not reported to credit bureaus, on-time payments may not improve scores. Defaults can still lead to legal actions or judgments that harm credit.

10. Do you need a lawyer for seller financing?

Yes. A real estate attorney should draft the promissory note, record the deed or land contract, and ensure compliance with all applicable laws to protect both parties.

Summary: What Is Seller Financing?

Seller financing (also known as owner financing or a purchase-money mortgage) is a real estate arrangement where the property seller acts as the lender instead of requiring the buyer to obtain a traditional bank mortgage. The buyer makes a down payment and then pays the seller in monthly installments, often with interest, until the balance is paid or refinanced.

This type of financing benefits buyers who may not qualify for conventional loans, as well as sellers who want to attract more buyers, close faster, and earn a steady income with interest. Common structures include promissory notes with a mortgage or deed of trust, land contracts (contract for deed), lease options (rent-to-own), wraparound mortgages, and even assumable mortgages in certain cases.

While seller financing offers flexibility, faster closings, and lower upfront costs, it also comes with risks such as higher interest rates, balloon payments, and potential default. For sellers, there is exposure to buyer nonpayment and legal restrictions, but also the potential for long-term financial gains.

In short, seller financing is an alternative path to homeownership and property sales that bypasses banks, offering unique opportunities and tradeoffs for both buyers and sellers.

Read Also: The Best Banks for Real Estate Investors

This FREE Training gives you the same system our students use to start fast and scale smart. Watch it today—so you can stop wondering and start closing.

*Disclosure: Real Estate Skills is not a law firm, and the information contained here does not constitute legal advice. You should consult with an attorney before making any legal conclusions. The information presented here is educational in nature. All investments involve risks, and the past performance of an investment, industry, sector, and/or market does not guarantee future returns or results. Investors are responsible for any investment decision they make. Such decisions should be based on an evaluation of their financial situation, investment objectives, risk tolerance, and liquidity needs.

👉FREE Training

How To Consistently Wholesale, Flip Houses, & Invest In Rental Properties From The MLS

(Without Spending $1 On Marketing)

Alex Martinez, the founder of Real Estate Skills, is known for his strong, practical expertise in real estate, starting from a beginner with no family connections in the industry to completing over 50 real estate deals, including wholesale and flips, within his first year.

He has dedicated his career to providing cutting-edge education and resources for real estate professionals. He emphasizes the importance of self-taught knowledge through mentors, books, and hands-on experience.

His journey from earning a modest income to becoming a successful real estate entrepreneur and educator showcases his expertise and dedication to the field.

Ryan Zomorodi, co-founder and COO of Real Estate Skills, leverages his experience from a diverse background in real estate investment, construction management, and entrepreneurship to provide comprehensive education in the real estate sector.

His expertise is rooted in hands-on experience, extensive industry knowledge, and a commitment to empowering others through education.

Ryan's journey reflects a blend of practical experience and entrepreneurial success, contributing to his role in developing a platform that educates and supports aspiring real estate professionals.

Read Ryan's Full Bio >>