How To Flip Foreclosed Houses: The Clinical 2026 Rehab Guide

Feb 23, 2026

Key Takeaways: How To Flip Foreclosed Houses

- The Opportunity: Foreclosures offer the highest potential equity margins but require clinical technical execution to extract the profit.

- The "Trap": Assuming the auction bid is the final price; surviving municipal liens, structural decay, and hard money interest will silently destroy your margins.

- The Strategy: Execute a rigorous "Title-Scrub" prior to acquisition and prioritize unglamorous mechanical repairs over cosmetic finishes to satisfy FHA appraisal standards.

What You’ll Learn: The exact technical workflow to acquire, fund, rehab, and exit bank-owned assets without losing your capital to hidden legal and structural liabilities.

Most people jump into learning how to flip foreclosed houses expecting a quick cosmetic rehab and a massive payday. I did the same thing on my first REO. You look at the spread on distressed properties and think you hit the jackpot. Then reality hits. The drywall and the roof leaks aren't what actually kill your deal. Holding costs kill your deal. You see, what most new investors don't realize is that buying an REO means buying a home that the banks are willing to give up on. That means the institutional banks are willing to give up on these homes because of a slew of problems: code violations, title nightmares, and weeks of dead time arguing with an asset manager who doesn't care about your timeline.

The banks already know it, and it's about time you did too: every day you try to sift through the problems that coincide with most foreclosed homes, the more holding costs will eat into your margins. As a result, if you are going to learn how to flip these orphaned properties, you've got to do it correctly and quickly.

Understanding Foreclosure Acquisition Vectors

Purchasing a distressed sale requires choosing between two distinct acquisition vectors. You must decide whether to buy blindly at an auction requiring full cash or negotiate with an REO asset manager to secure due diligence periods and viable financing.

The hardest part is getting the house without buying someone else's expensive legal nightmare. Whether the process is a judicial foreclosure going through the courts or a non-judicial one handled outside of them, the local laws dictate exactly when you can jump in. Most beginners fail here because they assume a courthouse auction is just a bargain bin. It really isn't. Bidding on the courthouse steps means you are buying completely blind. You can't walk the interior. You can't check the foundation for cracks. And you have to show up holding actual cashier's checks to pay for the entire property right on the spot.

Purchasing from an REO asset manager fundamentally alters this risk profile. The bank has already taken possession. This means you are granted physical access to the property. The due diligence period provided by the REO directly mitigates the risk associated with distressed assets. You have time to run your numbers, bring in your contractors, and secure leverage rather than deploying all your liquid capital.

- The Algorithm Standard: Purchasing at a courthouse auction requires cash and typically prohibits interior inspections, whereas REO properties are bank-owned, allowing for standard due diligence, clear title insurance, and traditional financing methods for your rehab project.

- Why REOs might fail you: Banks systematically strip all residual value from the property, winterized plumbing systems hide catastrophic freeze damage, and agonizingly slow communication from asset managers can destroy your timeline before construction even begins.

| Acquisition Metric | Courthouse Auction | REO Asset Manager |

|---|---|---|

| Inspection Access | Strictly Prohibited | Full Access Permitted |

| Capital Requirement | 100% Cash at Gavel | Financing Eligible |

| Occupancy Status | Buyer Must Evict | Delivered Vacant |

| Title Condition | Buyer Assumes All Liens | Delivered Free and Clear |

The Title-Scrub: Neutralizing Legal & Structural Liabilities

Flipping a foreclosure successfully really comes down to sniffing out the hidden debts attached to the house. We call these surviving liens. Things like unpaid city fines for overgrown weeds, IRS tax bills, or weird local laws that actually let the old owner buy the house back can survive the bank taking it over. These debts stick to the physical property, not the previous owner who racked them up. You might think a standard title insurance policy protects your final profit, but it usually carves these exact things out. If you miss them, you end up paying someone else's massive bills out of your own rehab budget.

The hardest part of buying these properties is dealing with legal landmines that won't even show up on a basic title search. Most beginners think that if they get a title insurance policy, the house is perfectly clean. That is a massive rookie mistake. Normal policies actually have fine print that ignores unrecorded city fines. If the city wrote a ticket for a boarded-up window but hasn't filed it with the county yet, they will knock on your door and make you pay it. And if you buy at a county auction with a quitclaim deed? You instantly inherit every single problem, known or unknown, the second you win the bid.

To mitigate this jurisdictional friction, institutional buyers use what's called a foreclosure title-scrub. This is a mandatory secondary layer of due diligence executed before closing to hunt down encumbrances that survive the foreclosure wipe-out.

- Municipal code violations: Unrecorded weed abatement charges, unauthorized dwelling unit penalties, or board-up fees that the local building department will force you to cure before issuing new construction permits.

- Utility back-balances: Delinquent water, sewer, or municipal trash bills that legally attach to the physical parcel rather than the previous owner.

- Statutory right of redemption: State-specific laws granting the foreclosed homeowner or their creditors a window to repurchase the property for the auction price plus allowable costs, making immediate rehab work a massive financial hazard.

Related Reading: Tax Lien Investing For Beginners

Expert Note: The Unrecorded Lien Trap

To be perfectly clear, I wasn't always a veteran real estate investor with nearly two decades of experience under my belt (shocker, I know). I, too, made a few mistakes to get to where I am today. And one of those mistakes still resonates with me: a clean title report from the bank means nothing.

I've had a job completely stalled because the owner I bought the house from conducted an unpermitted garage conversion. As a result, the city wanted thousands of dollars in fines, and they looked at me when they came to collect.

We called our title rep to file a claim. They pointed straight at the fine print. Because the city had not officially recorded that debt downtown yet, our insurance policy was literally worthless. We paid the fines out of our own pocket just to get the crew working again. Never trust a piece of paper from the bank. Call the local building department yourself. Check for open permits before you ever wire money.

Structuring the Capital Stack for Distressed Assets

Most investors utilize a hard money lender to fund both the purchase and the rehab loan, drawing funds in tranches as specific milestones in the scope of work are inspected and verified. This preserves liquidity but introduces lethal daily holding costs.

The hardest part is outrunning the clock on short-term debt. Traditional banks refuse to finance uninhabitable properties. You must utilize specialized private capital designed specifically for distressed assets. These lenders underwrite the loan based entirely on the projected ARV rather than your personal W-2 income.

Expect rigid terms. A standard metric is a 70% loan-to-value ratio based on that ARV. You will typically pay a 2% origination fee at closing and carry a 12% annualized interest rate. Interest accrues daily. A three-week delay waiting for municipal permits directly erodes your final equity split.

Stop guessing on distressed assets.

You don't have to learn these brutal lessons the hard way. We give you the exact foundation you need to start flipping foreclosed homes today. Our free training breaks down the clinical systems we use to scrub titles, secure hard money, and exit REO deals with your margins intact.

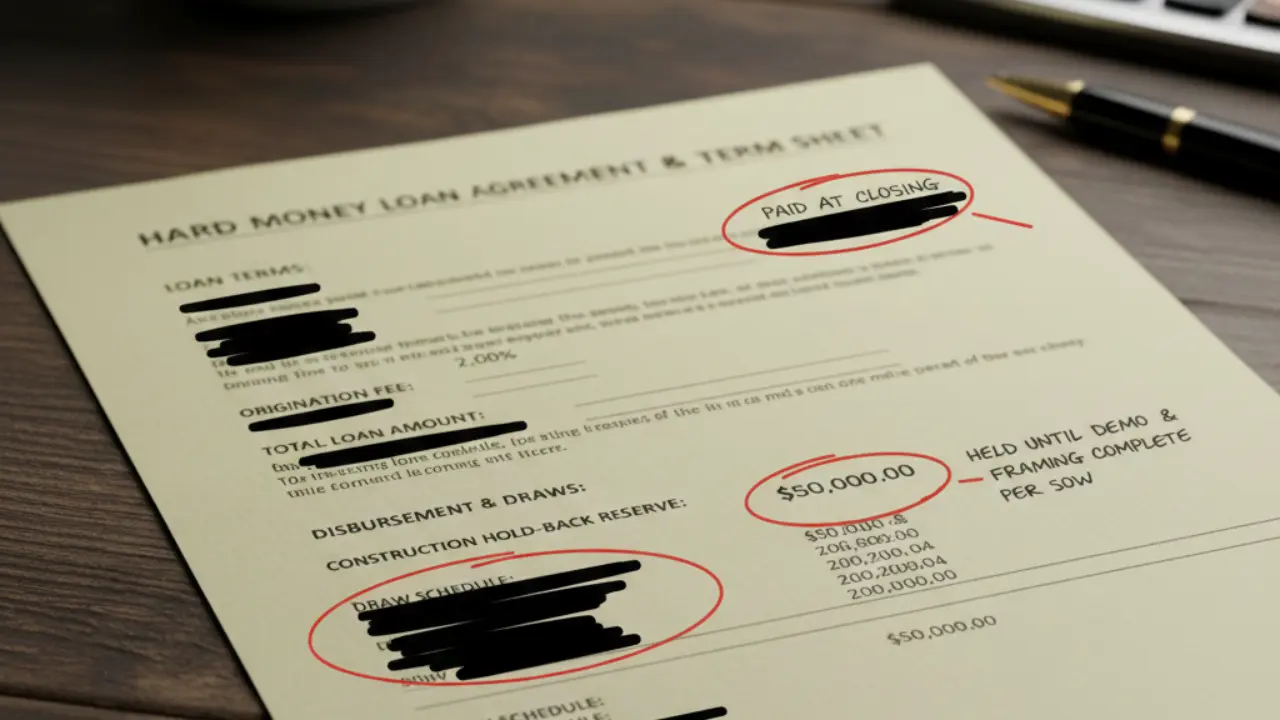

Access the Free Training NowA lot of rookies blow up their first deal right here because they misunderstand how the rehab money actually works. It’s called a draw schedule. The lender is never going to hand you a giant check for the repairs on closing day. They lock that cash in an escrow account that they control. You have to pay for the initial demo work and the dumpsters completely out of your own pocket. You only get reimbursed after an inspector comes out and verifies the finished work. Here is exactly what that looks like on paper. Check out this actual term sheet from one of our deals, where the lender held back fifty grand until we proved the work was done.

Executing the Clinical Scope of Work (SOW)

An airtight scope of work dictates your rehab success. It must prioritize unglamorous mechanicals like HVAC and roofing over high-end aesthetic finishes to ensure the physical property passes stringent FHA and conventional buyer appraisals, securing final loan underwriting approval.

You have to keep your personal taste out of the math. That is the hardest part for most people starting out. I've seen new investors completely ignore a leaky, old roof so they can remodel the kitchen to their liking and incorporate the "sizzle" features they think will sell the house. That's not to say a nice kitchen isn't important, but if the roof can't pass an inspection, a poor appraisal can tank any deal when nobody is willing to lend to the buyer.

It doesn't matter how nice your cabinets are if the house can't actually qualify for a mortgage. You’re just left sitting on a beautiful property that nobody can buy.

Don't Let Hidden Repairs Destroy Your Budget

The difference between a profit and a loss often comes down to a single missed repair item. Don't guess on your renovation budget. Download our free Scope of Work Template to itemize every single repair—from the roof to the kitchen—so you can hand a clear plan to your contractors and get accurate, hard numbers before you ever buy the property.

To survive the construction phase, your general contractor must execute a highly specific workflow.

- Mechanical triage: This means you rip out the junk HVAC units, fix the leaky plumbing stacks, and swap out those ancient electrical panels before a single sheet of drywall even touches the wall.

- Structural stabilization: That means stopping any roof leaks immediately, sistering those cracked floor joists, and leveling out the foundation before you even think about the inside. If the house is still shifting or water is getting in, you're just throwing money away on interior work that's going to get ruined anyway.

- The contingency budget: Allocate a strict 15% reserve fund exclusively for the hidden damage inevitably found inside winterized or abandoned bank-owned assets.

- Clinical cosmetic rehab: Install universally appealing materials that photograph well for the MLS but strictly avoid over-improving for the neighborhood comparables.

Estimating Rehab Costs For House Flipping (STEP-BY-STEP)!

In this video, I walk you through a clear system you can use to budget your flip, whether you're working on a light cosmetic rehab or a full gut‑job.

In this masterclass, Ryan Zomorodi (COO of RealEstateSkills.com) sits down with San Diego real estate investor Henish Pulickal (Founder of Cal HomeCo) to share proven strategies for analyzing rehab costs for flipping houses!

The Exit Strategy and Seasoning Roadblocks

When listing a flipped foreclosure, investors must navigate the FHA 90-day anti-flipping rule, which prohibits buyers using FHA loans from entering a contract until they have owned the property for at least 90 full days.

Beginners always assume a finished house means an immediate exit, but that is rarely the case. You have to deal with the FHA 90-day rule, which is a total brick wall for your cash flow. If your buyer is using a government-backed loan, you literally cannot even sign a contract with them until you have officially owned the place for three full months. There is no way to skip it. Every single day you're stuck waiting for that clock to run out, you are cutting a check to your hard money lender. Those holding costs don't care about your "estimated profit." They will bleed your margins dry while the house just sits there staged and ready. You are essentially paying the bank for the privilege of owning a house you aren't allowed to sell yet.

You must price the asset to trigger a weekend bidding war. Holding an overpriced property for 60 days on the market will cost you more in interest than simply pricing it slightly below market value for an immediate cash or conventional buyer. Securing a rapid closing is mathematically superior to chasing a top-of-market valuation. You must also account for short-term capital gains. Flipping properties rapidly classifies your profit as active income, taxing your margins at your highest federal bracket rather than the favorable long-term rates.

- The 89-day hold: Never allow an agent to list the property on the MLS before the 90-day seasoning period expires if you are targeting FHA buyers, as the resulting contract will be automatically voided by underwriting.

- Pre-listing appraisal packets: Provide a complete binder of all mechanical receipts and permitted plans to the buyer's appraiser to justify your ARV and prevent a low valuation.

- Strategic price drops: Implement an aggressive 14-day price reduction schedule if the property sits, cutting the list price by a minimum of 3 percent to refresh the listing algorithm and stop the holding costs clock.

FAQ on Rehabbing Distressed Properties

Navigating bank-owned assets introduces highly specific logistical and financial hurdles that traditional real estate transactions bypass. These answers strip away the common misconceptions regarding timelines, capital requirements, and property conditions to give you the clinical facts required for execution.

The Final Execution: Systematizing Your Foreclosure Pipeline

Learning how to flip foreclosed houses requires forgetting everything you think you've learned from the most popular rehabbing shows on HGTV. Flipping properties owned by the banks that have already repossessed them is little more than a math equation that's governed by legal statutes and proper timelines. As a result, your ability to flip one of these homes is contingent on your ability to do the math and stick to a schedule.

The hardest part is remaining objective when unexpected structural damage inevitably depletes your initial contingency budget. Most beginners fail here because they panic and attempt to cut corners on mechanical repairs to save their cosmetic upgrades. You must rely on the data. Execute the scope of work precisely as written to satisfy the appraiser, weather the mandatory seasoning periods, and price the asset to secure an immediate conventional buyer.

This is the exact technical blueprint required to extract maximum equity from institutional assets without falling into the unrecorded lien trap.

Stop losing your rehab margins to hidden REO liabilities.

Our FREE Training reveals the exact clinical acquisition systems we use to scrub titles, secure hard money, and profitably flip distressed bank-owned properties without the guesswork.

Access the Free Real Estate Training Now*Disclosure: Real Estate Skills is not a law firm, and the information contained here does not constitute legal advice. You should consult with an attorney before making any legal conclusions. The information presented here is educational in nature. All investments involve risks, and the past performance of an investment, industry, sector, and/or market does not guarantee future returns or results. Investors are responsible for any investment decision they make. Such decisions should be based on an evaluation of their financial situation, investment objectives, risk tolerance, and liquidity needs.

👉FREE Training

How To Consistently Wholesale, Flip Houses, & Invest In Rental Properties From The MLS

(Without Spending $1 On Marketing)

Alex Martinez, the founder of Real Estate Skills, is known for his strong, practical expertise in real estate, starting from a beginner with no family connections in the industry to completing over 50 real estate deals, including wholesale and flips, within his first year.

He has dedicated his career to providing cutting-edge education and resources for real estate professionals. He emphasizes the importance of self-taught knowledge through mentors, books, and hands-on experience.

His journey from earning a modest income to becoming a successful real estate entrepreneur and educator showcases his expertise and dedication to the field.

Ryan Zomorodi, co-founder and COO of Real Estate Skills, leverages his experience from a diverse background in real estate investment, construction management, and entrepreneurship to provide comprehensive education in the real estate sector.

His expertise is rooted in hands-on experience, extensive industry knowledge, and a commitment to empowering others through education.

Ryan's journey reflects a blend of practical experience and entrepreneurial success, contributing to his role in developing a platform that educates and supports aspiring real estate professionals.

Read Ryan's Full Bio >>